Risks 2024, 12(4), 68; https://doi.org/10.3390/risks12040068 - 17 Apr 2024

Abstract

Portfolio diversification is an accepted principle of risk management. When constructing an efficient portfolio, there are a number of asset classes to choose from. Financial innovation is expanding the range of instruments. In addition to traditional commodities and securities, other instruments have been

[...] Read more.

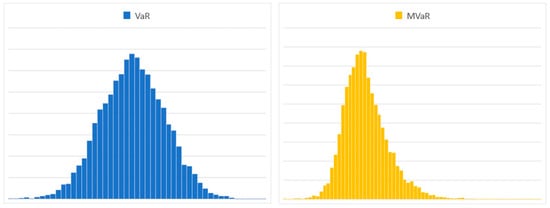

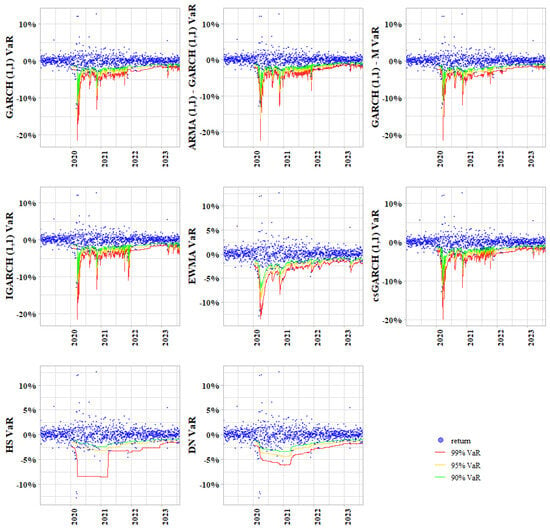

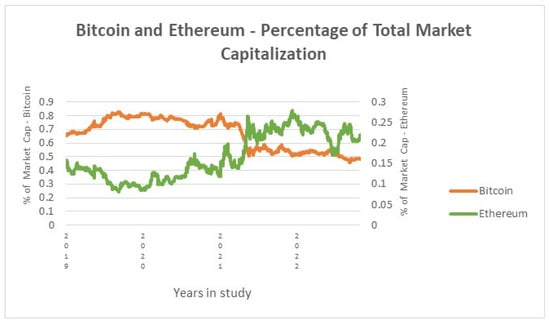

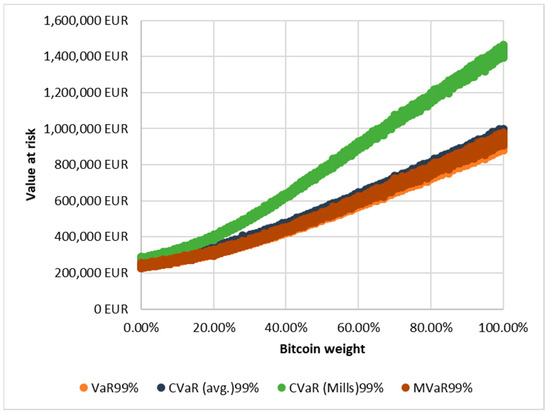

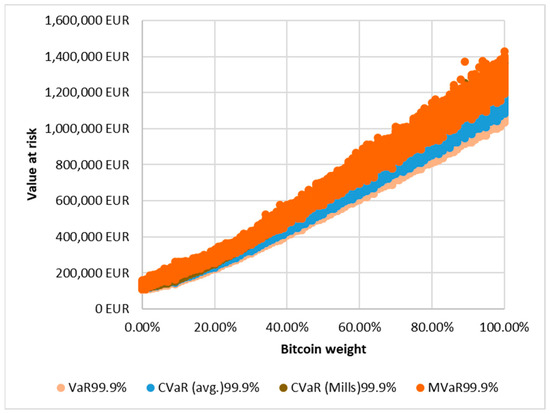

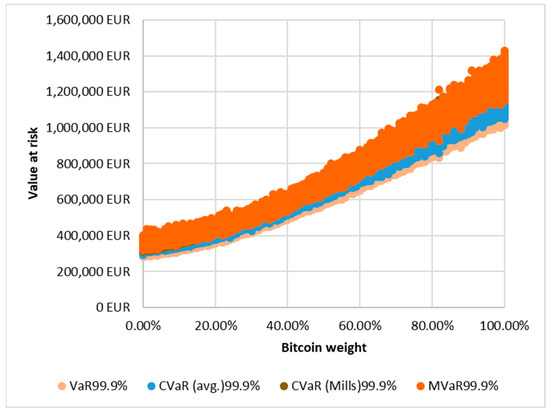

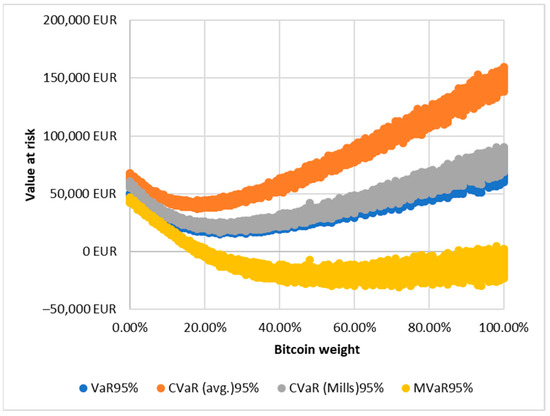

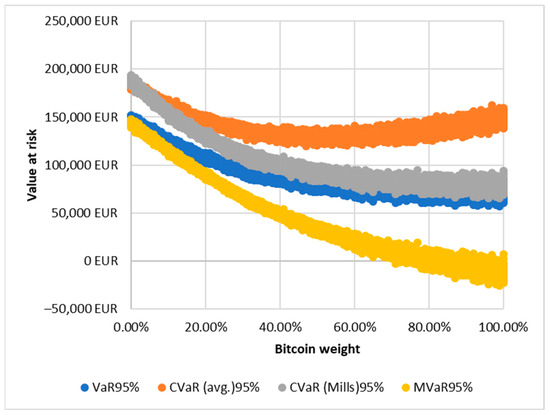

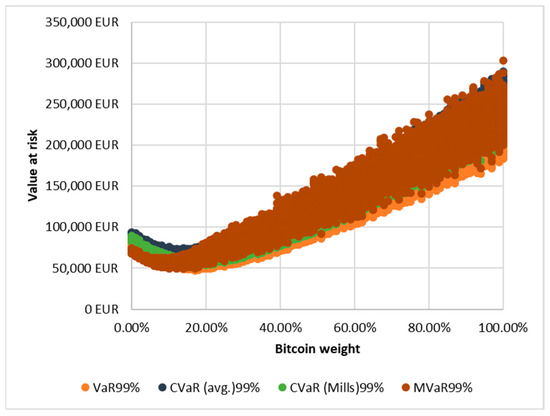

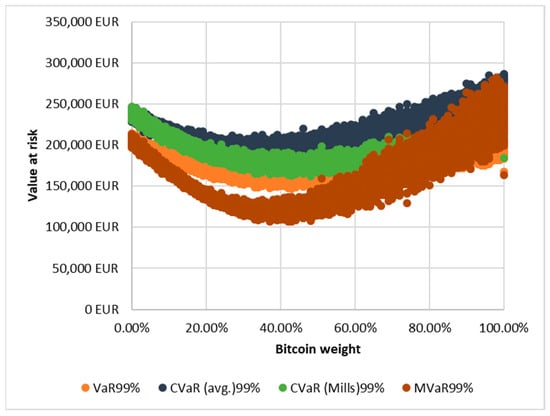

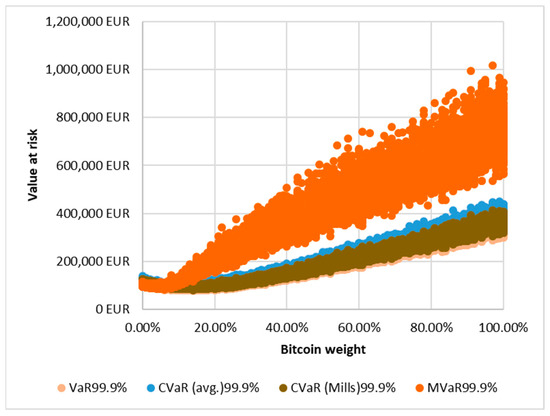

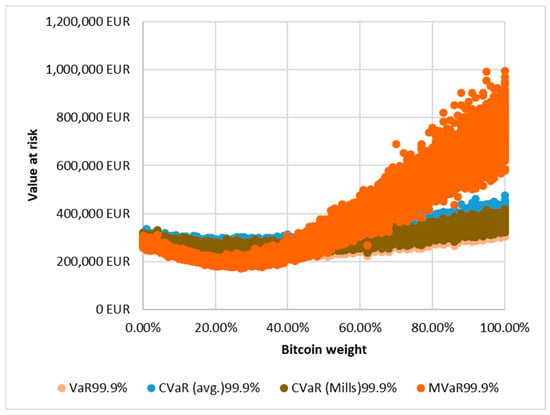

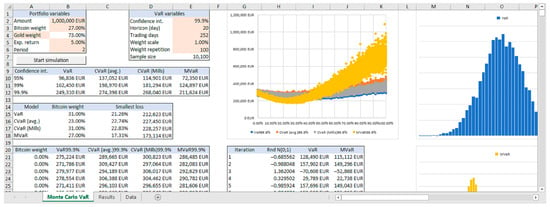

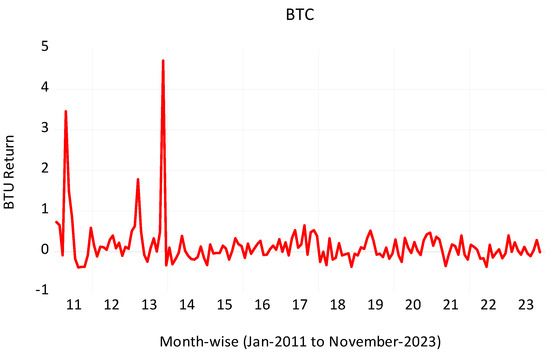

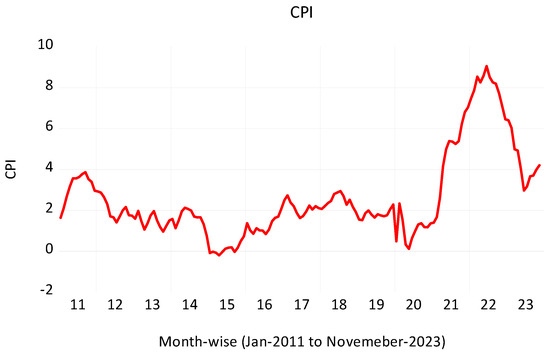

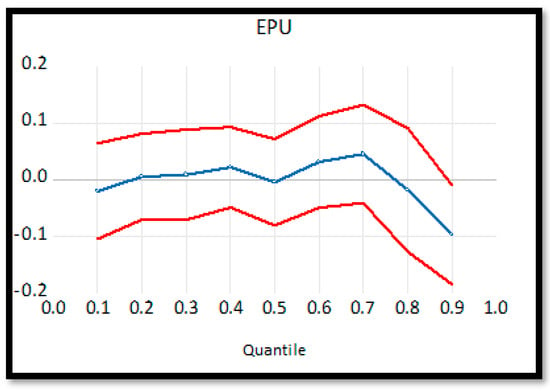

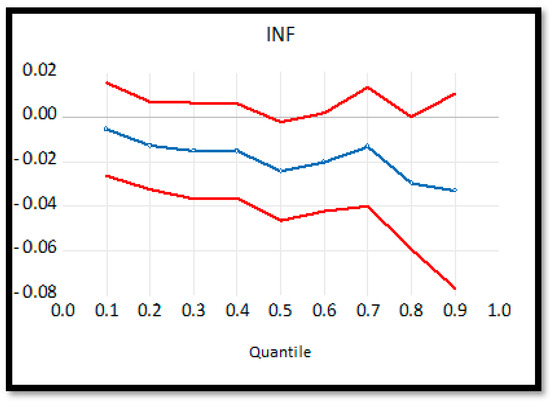

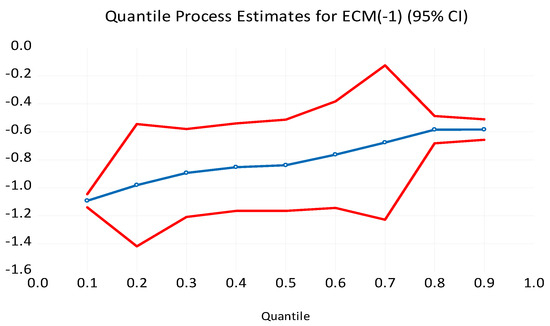

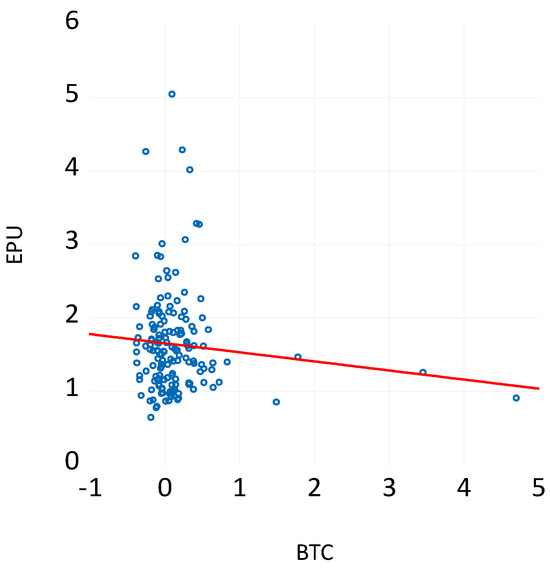

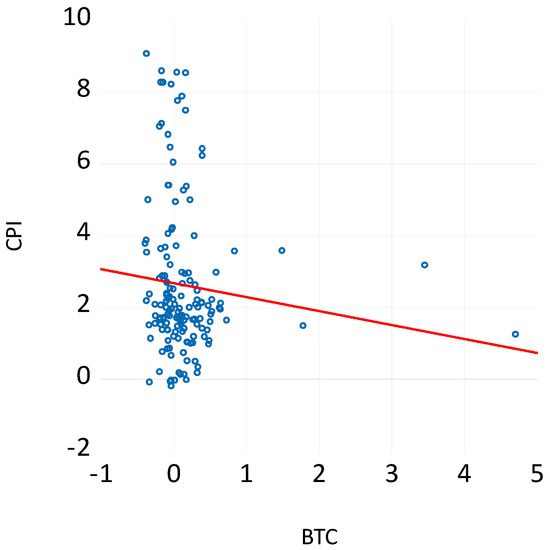

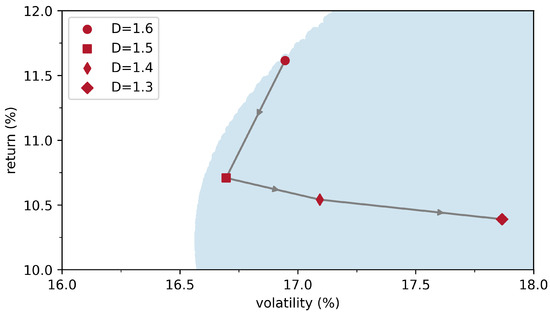

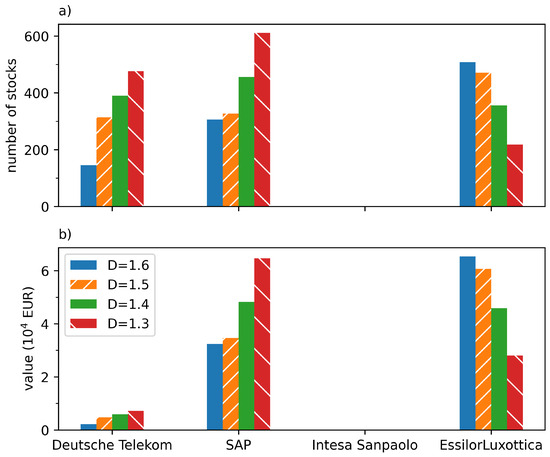

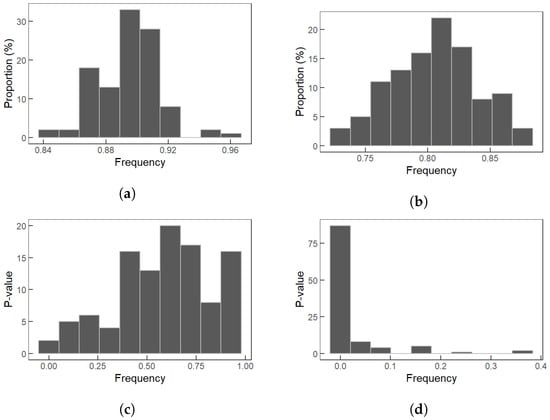

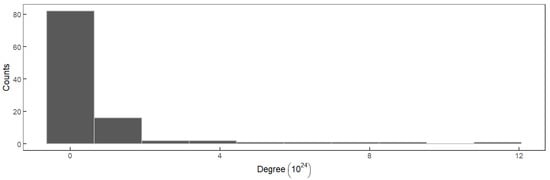

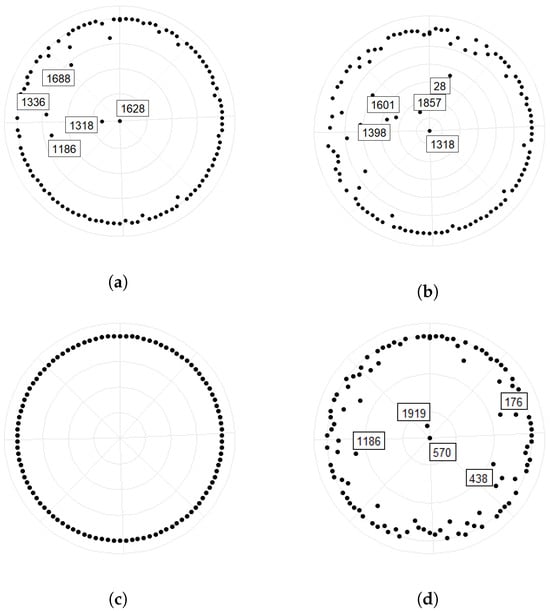

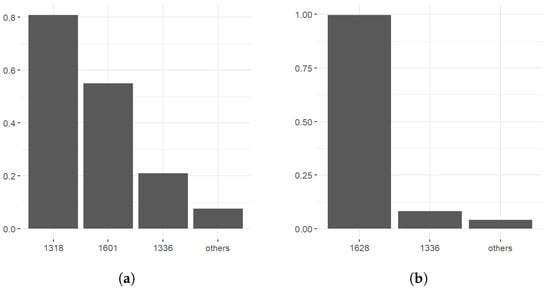

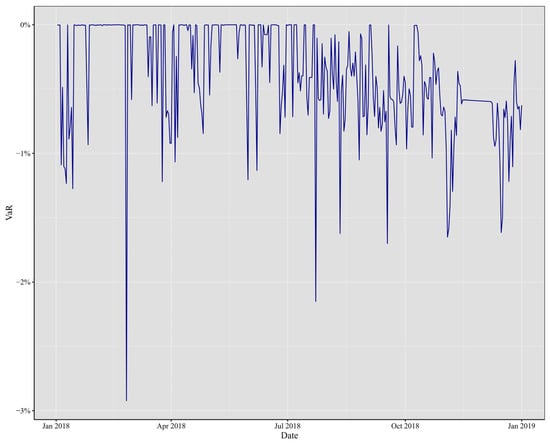

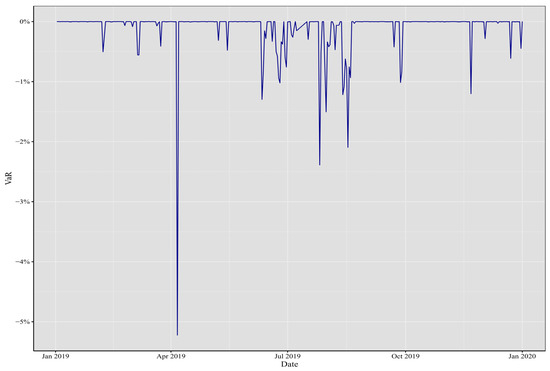

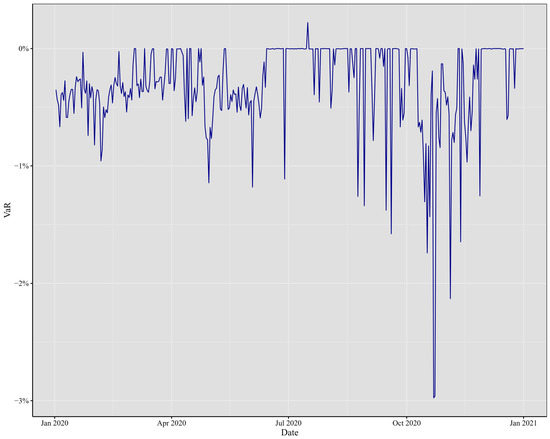

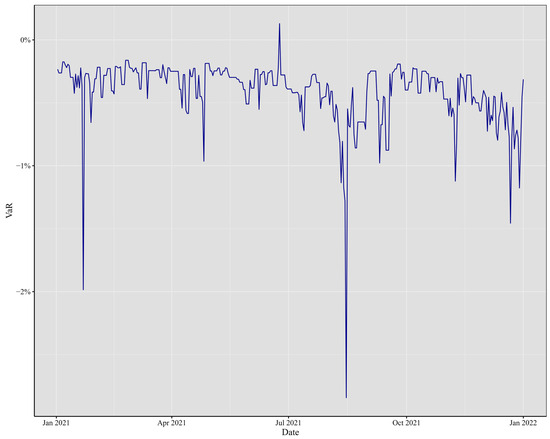

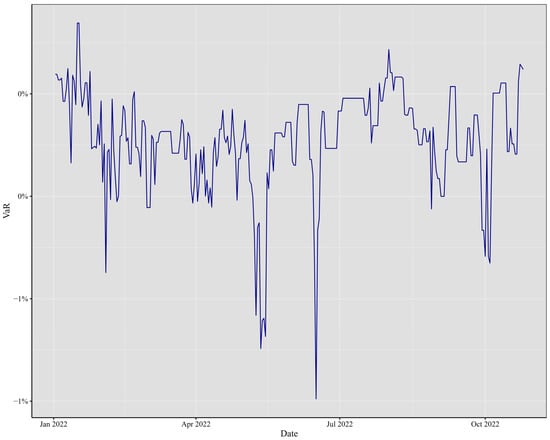

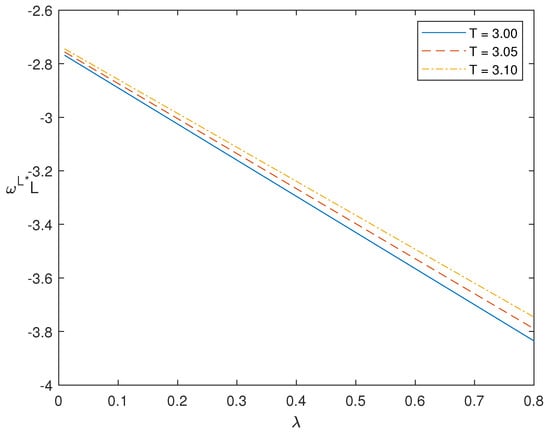

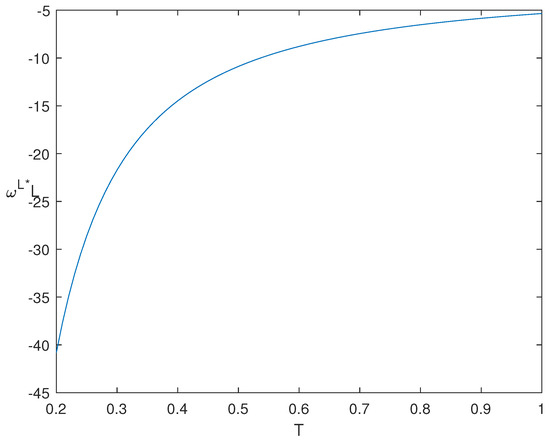

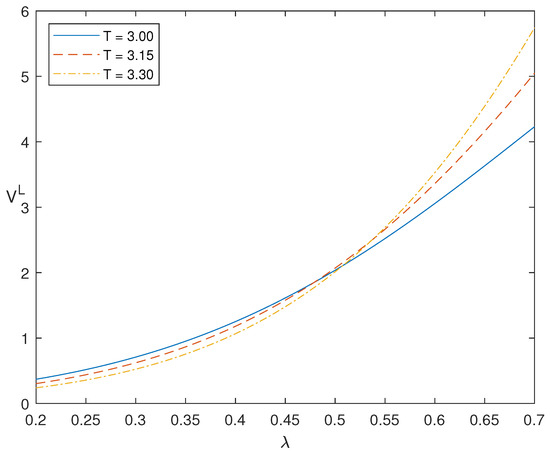

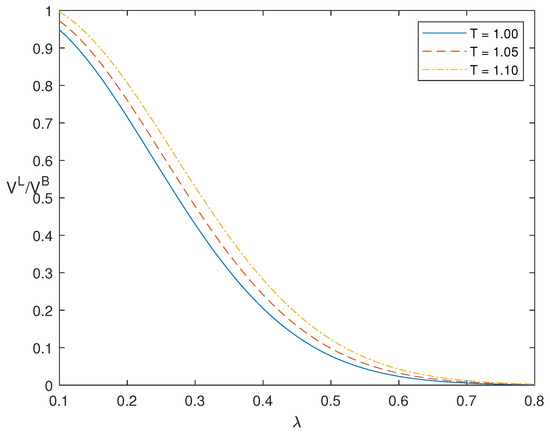

Portfolio diversification is an accepted principle of risk management. When constructing an efficient portfolio, there are a number of asset classes to choose from. Financial innovation is expanding the range of instruments. In addition to traditional commodities and securities, other instruments have been added. These include cryptocurrencies. In our study, we seek to answer the question of what proportion of cryptocurrencies should be included alongside traditional instruments to optimise portfolio risk. We use VaR risk measures to optimise the process. Diversification opportunities are evaluated under normal return distributions, thick-tailed distributions, and asymmetric distributions. To answer our research questions, we have created a quantitative model in which we analysed the VaR of different portfolios, including crypto-diversified assets, using Monte Carlo simulations. The study database includes exchange rate data for two consecutive years. When selecting the periods under examination, it was important to compare favourable and less favourable periods from a macroeconomic point of view so that the study results can be interpreted as a stress test in addition to observing the diversification effect. The first period under examination is from 1 September 2020 to 31 August 2021, and the second from 1 September 2021 to 31 August 2022. Our research results ultimately confirm that including cryptoassets can reduce the risk of an investment portfolio. The two time periods examined in the simulation produced very different results. An analysis of the second period suggests that Bitcoin’s diversification ability has become significant in the unfolding market situation due to the Russian-Ukrainian war.

Full article

(This article belongs to the Special Issue Risk Analysis in Financial Crisis and Stock Market)

►

Show Figures

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}